Whole Life vs. Term Life Insurance: What the Math Actually Shows

For most Americans, term life insurance is the right choice. It covers you when you need it most, costs a fraction of what whole life costs, and frees up capital to be invested and compounded over time. At Freedom Capital Advisors, a Florida-registered investment adviser, we work with families and retirees who come to us having paid into whole life policies for years, wondering why their “investment” never grew the way they were promised.

The answer usually comes down to math and incentives, and neither one favors the buyer of a whole life policy.

Term life is exactly what it sounds like: coverage for a defined term (10, 20, or 30 years) at a locked-in monthly premium. Whole life covers you permanently and builds a “cash value” component that your agent will describe as a savings or investment vehicle, often making this cash value sound like it could be your entire retirement plan.

Here is the problem. That cash value comes at a steep cost, and when you run the numbers side by side, the argument for whole life collapses for the majority of people.

What Is Term Life Insurance?

Term life insurance is the most straightforward form of life coverage available. You pay a monthly premium, and if you die during the coverage period, your beneficiaries receive the death benefit. When the term ends, the policy expires.

That simplicity is a feature. A healthy 35-year-old can lock in a 20-year, $500,000 term policy for roughly $25 to $40 per month, based on current rates from major carriers (MoneyGeek, 2026) The premium is predictable, the coverage is substantial, and nothing is buried in the fine print.

Most financial planners use a simple framework: you need life insurance most when you have dependents, a mortgage, and significant income to replace. That window typically runs from your late 20s through your mid-50s. Term life covers that window precisely and affordably.

What Is Whole Life Insurance?

Whole life insurance covers you for your entire life and includes a cash value component that grows over time. A portion of every premium goes toward the death benefit and insurer fees. A smaller portion is credited to your “cash value” account, which you can borrow against or surrender.

That same $500,000 policy for a healthy 35-year-old runs approximately $300 to $500 per month in whole life premiums, roughly 9 to 10 times the cost of term (MoneyGeek, 2026). Some policies run higher.

Whole life agents will emphasize the permanent coverage and cash value growth. What they spend less time on is the cost comparison and what that cash value actually returns over decades.

The Math That Most People Never See

This is where the conversation shifts.

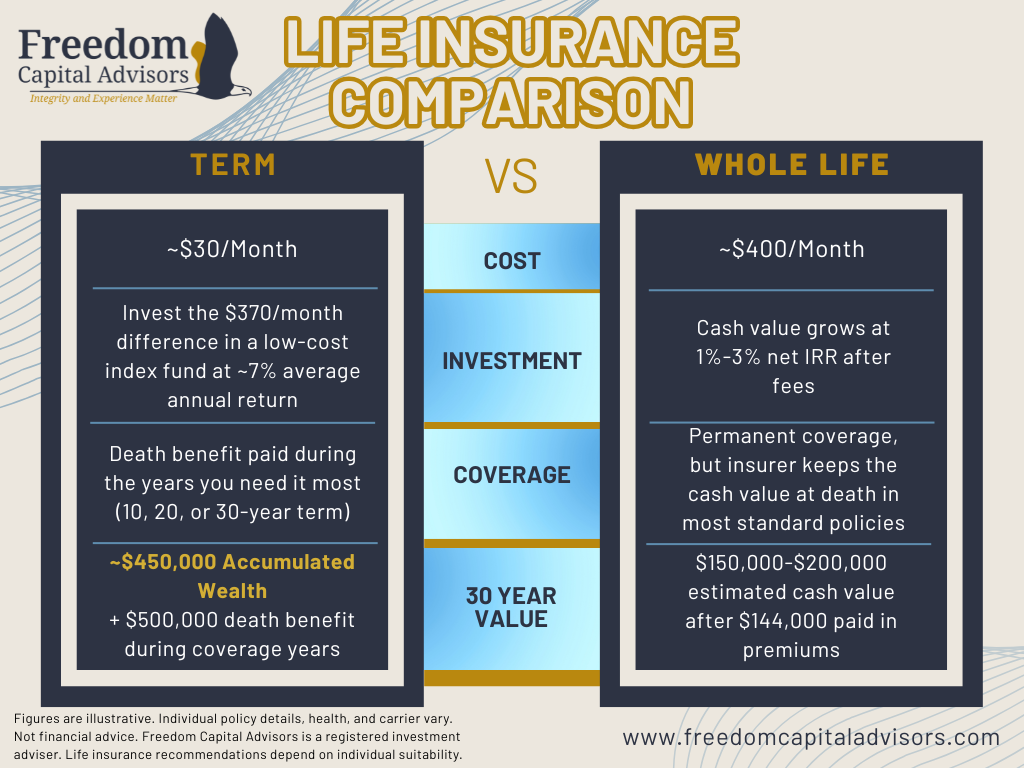

Using conservative round numbers: a term policy costs about $30 per month and a comparable whole life policy costs about $400 per month. The difference is $370 per month.

If you invested that $370 every month in a low-cost index fund earning a 7% average annual return (a conservative long-term proxy for broad market performance), here is what happens over 30 years:

You would accumulate approximately $450,000.

Thirty years of whole life premiums at $400 per month equals $144,000 paid in. The cash value on a whole life policy at that point, after fees, typically carries an internal rate of return of 1% to 3% net. You might walk away with $150,000 to $200,000 in cash value.

Compare that to $450,000 built through the “buy term, invest the difference” approach, with a $500,000 death benefit still in place during the years you needed coverage most.

The math favors term. By a significant margin.

These are illustrative figures and individual policy details vary, but the directional story they tell is consistent across virtually every comparison we run.

Why Whole Life Gets Sold So Often

This is the part of the conversation that does not get enough attention.

Life insurance agents who sell whole life policies earn significantly higher commissions than agents selling term. A typical whole life commission in year one is 50% to 100% or more of the annual premium. On a $400 per month policy, that is $2,400 to $4,800 in the first year alone. The same agent selling a $30 per month term policy might earn $100 to $200.

This creates an obvious conflict of interest. The agent earns more by recommending the more expensive product, regardless of whether that product is right for the client.

It is the same structural problem we see in annuity sales, where commission-based advisors push products that generate the highest payout to them rather than the best outcome for the client. We have written about how this plays out with annuities as well. When compensation is tied to the product sold rather than the quality of the advice, suitability takes a back seat.

A fee-only fiduciary has no financial incentive to steer you toward one product over another. The recommendation is based on what fits your situation, not what pays the most at signing.

When Whole Life Insurance Actually Makes Sense

Whole life is not the right tool for most people, but there are situations where permanent coverage serves a legitimate purpose.

Estate planning for high-net-worth individuals. If your estate is large enough to trigger estate taxes, a whole life policy held inside an irrevocable life insurance trust can provide liquidity to cover the tax bill without forcing your heirs to sell assets.

Business succession planning. Buy-sell agreements between business partners often use permanent life insurance to fund a buyout if one partner dies. Permanent coverage aligns with the indefinite nature of a business relationship.

Special needs planning. Families supporting a dependent with special needs may need coverage that does not expire. A permanent policy can fund a special needs trust regardless of when the insured passes.

Uninsurability. In rare cases, someone may not qualify for new term coverage later in life due to health conditions. If you are already locked into a whole life policy and are now uninsurable, surrendering it may not be the right move.

These are edge cases. They apply to a small percentage of the population. For the majority of working families and investors with investable assets, term life covers the need at a fraction of the cost.

What Fiduciaries Recommend and Why

A fiduciary is legally required to act in your best interest, not their own. That legal standard changes the recommendation.

When a fiduciary advisor evaluates life insurance, the analysis starts with what the coverage needs to accomplish: income replacement, debt coverage, and protection for dependents during the years you are building wealth. Term life addresses all of those needs cleanly.

The cash value component of whole life is not competitive with the market as an investment vehicle. Life insurance is not an investment account. When you treat it as one, you pay a significant premium for a return that a diversified portfolio would beat consistently over time.

The fiduciary recommendation is almost always term. Buy coverage for the period you need it. Invest the difference.

If you want a second opinion on a policy you are currently holding, or want to talk through what coverage actually makes sense for your situation, we offer complimentary consultations.

Frequently Asked Questions

Is whole life insurance ever a good investment?

For most people, no. The internal rate of return on whole life cash value, after fees and the cost of insurance, typically runs between 1% and 3% over the long term. A low-cost index fund has historically returned 7% or more on an inflation-adjusted basis. The cash value component of whole life underperforms the market over nearly every comparable time horizon.

Why do so many financial advisors recommend whole life insurance?

Many people who sell life insurance are not fiduciaries. They are commission-based agents who earn significantly more by selling whole life than term. The incentive structure favors the more expensive product. A fee-only fiduciary advisor has no financial incentive to push whole life and will recommend term based on your actual coverage needs.

What happens to the cash value when you die with a whole life policy?

In most standard whole life policies, the insurance company keeps the cash value. Your beneficiaries receive only the stated death benefit, not the death benefit plus the cash value you spent decades accumulating. This is a detail many policyholders do not learn until it is too late.

How much term life insurance do I actually need?

A common rule of thumb is 10 to 12 times your annual income, though your actual need depends on your debts, dependents, existing assets, and income replacement timeline. A fiduciary advisor can walk through the calculation based on your specific situation.

Should I cancel my existing whole life policy?

Not necessarily, and the right answer depends on your specific policy details. If you are uninsurable, have significant cash value built up, or have a legitimate estate planning need, surrendering may not make sense. If you are paying into a policy that does not serve a clear purpose, it is worth a second opinion. We offer complimentary consultations at Freedom Capital Advisors.